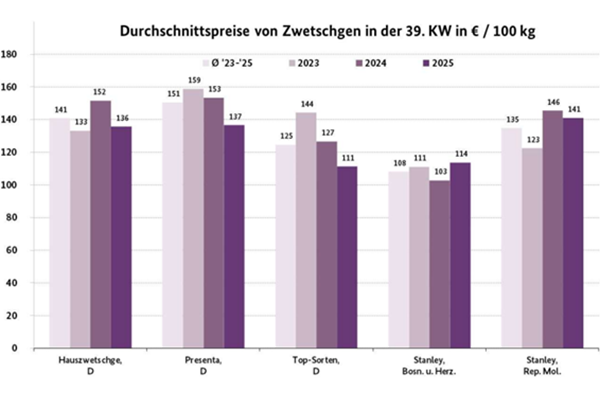

According to the German BLE, the season is coming to an end, with availability apparently limited. Domestic plums and prunes in the form of Presenta, Hauszwetschge, and various Top varieties played the leading role alongside Stanley from Eastern Europe. The quality was generally still impressive. The favorable weather improved storage conditions in Hamburg, allowing retailers to raise their prices slightly.

In Berlin, imports from Eastern Europe were popular, while domestic loads were difficult to sell. In Frankfurt, distributors raised their prices, but this immediately led to a slowdown in sales. There, a fairly wide price range established itself for the Top varieties, depending on the size of the fruit.

Plums were mostly available from France, Italy, and Spain. Here, prices developed quite unevenly amid quiet trading.

© BLE

© BLE

Click here to go directly to the full market and price report.

Apples

Domestic offers continued to be the focus, with Elstar, Jonagold, Wellant, and Boskoop forming the basis of the supply. Honeycrunch gained in importance, while the presence of early apples decreased. Royal Gala, Granny Smith, and Golden Delicious were the main varieties from Italy, with Kanzi, Pink Lady, and Red Delicious also being delivered in increasing quantities.

Pears

Turkish Santa Maria and Italian Abate Fetel, Williams Christ, and Santa Maria dominated the market. The presence of Xenia from the Netherlands and Germany increased. Marketing was unspectacular, with demand being met without any problems.

Table grapes

Italian deliveries dominated, with a wide range of varieties available. Italia, Michele Palieri, and Red Globe were the main varieties available, but late varieties such as Autumn Crisp and Autumn Pearl were also increasingly in stock. Red-skinned Turkish Crimson Seedless gained in importance.

Lemons

South African Eureka lemons dominated, but their quality was not consistently convincing, which led to significant price reductions in Hamburg. Falling prices were also observed in Berlin, where retailers wanted to minimize their South African stocks.

Bananas

Storage facilities had improved in various ways. In Munich, retailers subsequently increased their demands for second and third brands. Prices on other markets did not change significantly.

Cauliflower

Domestic produce predominated, flanked by Belgian and Polish loads. Availability was sufficient to meet demand, although storage facilities had improved in some places.

Lettuce

Lettuce came from Germany and Belgium, while mixed salad leaves came from Germany and Austria. Iceberg lettuce was available from German, Dutch, and Spanish suppliers. Marketing proceeded without any particular incidents.

Cucumbers

In the cucumber segment, the presence of Spanish loads apparently expanded: after only small quantities were available in the previous week, these loads now played a significant role. The increased supply inevitably had consequences for the prices of German, Dutch, and Belgian competitors.

Tomatoes

Belgian and Dutch deliveries dominated. Deliveries from Poland and Italy followed in terms of importance. Turkish imports increased, especially in the round tomato sector. The Spanish campaign got off to a slow start.

Sweet peppers

Supplies from the Netherlands prevailed, with Polish and Turkish supplies playing the main roles behind them. The presence of Spanish loads grew, which led to discounts from competitors in many places. Domestic and Belgian loads complemented the scene.